Climbing the Capital Gain Tax Pyramid to Lower Taxes

by Tim Voorhees and Dave Holaday

- The Federal capital gain tax rate is 20% for single taxpayers with taxable income over $415,050. For married taxpayers filing jointly, the threshold is $466,950. Many of these individuals have passive income subject to the Net Income Investment tax of 3.8% and the phase-out of deductions that can raise marginal tax rates by 1.2%. Add state tax rates that typically range from 5% to 13.3% and it not uncommon to see clients losing 25% to 35% to capital gain taxes.

- For many Americans selling a business or investment real estate may be the largest single financial transaction of their lives.

- Financial and legal professionals can help prospects and clients minimize unnecessary income taxes by climbing up a "tax efficiency" pyramid to realize greater benefits at each higher level.

- The most powerful capital gain tax planning strategies typically, 1) generate income tax deductions in the current year; 2) avoid capital gain taxes on sale; 3) provide a tax-exempt investment environment for reinvested sales proceeds and 4) produce tax-favored distributions.

- The most effective planning instruments typically involve the integration of legal, investment and insurance strategies. Collaboration among professional advisers is more important than ever.

- Family offices, because of their key role in coordinating professional advisers, are often called to quarterback the income tax planning transactions.

Opportunities for family offices increased dramatically in early 2013 when the President signed the American Tax Relief Act of 2012 into law. While the demand for estate planning shrank when the estate and gift tax exemption increased from $1 million per person to the new "permanent" exemption of more than $5 million per individual; the need for income and capital gain tax planning grew substantially.

The impact of the new higher tax rates is evident when projecting retirement cash flows generated by the sale and reinvestment of a capital asset. For example, a business owner selling a business valued at $3,000,000 might expect to pay about $850,000 in federal and state capital gain taxes. If the client was able to reinvest the cash proceeds and generate a 6.5% annual yield subject to a 30% blended tax rate, the result would be about $98,000 of annual retirement income. If instead, the client could avoid the capital gain tax on sale and avoid the income taxes on the reinvested proceeds, the result could be as much as $195,000. Planners who help clients move up the capital gain tax planning pyramid can have a dramatic positive effect.

To illustrate the hypothetical impact of reducing capital gain taxes over time, consider a client who sells an asset worth $3 million with a zero cost basis in a 30% tax environment. In Scenario 1 as indicated in Table 1 below, the client avoids the capital gain tax on sale and also invests the proceeds tax-efficiently to avoid tax on future reinvested earnings assumed to be 6.5%. In Scenario 2, the client avoids the capital gain tax but reinvests the proceeds in a conventional investment portfolio earning 6.5% and subject to an average income tax rate of 30%. In Scenario 3, both the sale and the 6.5% annual earnings on reinvested sale proceeds are subject to a 30% tax rate.

| Impact of Taxes on Sales and Reinvested Sale Proceeds | Immediate after-tax Sale Proceeds | Net Spendable Income over 20 Years @ 6.5% | Net Spendable Income over 30 Years @ 6.5% |

|---|---|---|---|

| Scenario 1: Tax-exempt sale and tax-free reinvestment earnings | $3,000,000 | $3,900,000 | $5,850,000 |

| Scenario 2: Tax-exempt sale and taxable reinvestment earnings | $3,000,000 | $2,730,000 | $4,095,000 Scenario 3: |

| Scenario 3: Taxable sale and taxable reinvestment earnings | $2,100,000 | $1,911,000 | $2,866,500 |

Table 1. Impact of Taxes on Sales and Reinvested Sale Proceeds

Obviously, Table 1 uses hypothetical data and simply serves to reinforce the importance of giving adequate consideration to tax-wise strategies for selling and reinvesting. Clearly, investments will perform better if taxes can be reduced or eliminated. Fortunately, there are a wide variety of planning instruments that can facilitate the tax-efficient disposition of assets, some of which will be discussed on the following pages. Moreover, taw laws allow for the integration of legal, investment, and insurance tools to facilitate tax-efficient accumulation and distributions. As long as clients are willing to make longer-term investments and properly integrate planning instruments, they can climb a pyramid with each higher level allowing for income tax deductions, tax-favored sales, tax-efficient investment compounding and tax-free income payments during retirement.

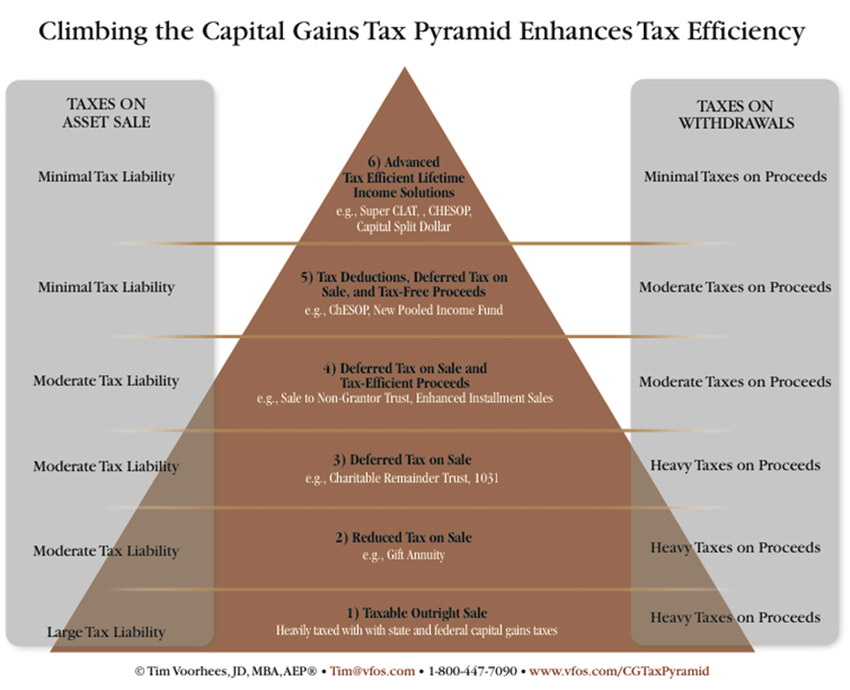

The Capital Gains Tax Pyramid in Figure 2 attempts to condense and organize a highly complex set of concepts into a single illustration with the purpose of clarifying the relationship between basic planning strategies and more tax-efficient strategies.

Figure2.Tax-Efficiency Pyramid

Sorting through the different tax planning options may seem daunting; however, the pyramid diagram helps to simplify the decision-making process. The six levels of the pyramid graphic, explained below, illustrate how clients are rewarded for advancing from traditional to more innovative strategies.

Level 1: The bottom level on the pyramid depicts how most clients sell assets. Their 1099’s report significant gains and they have no means to reduce or defer taxes and no offsetting tax deductions. Moreover, they reinvest the sale proceeds in portfolios that generate earnings which are also subject to taxes, as indicated on the right side of the pyramid below. Obviously, clients need to find more tax-wise solutions!

Level 2: Climbing the pyramid to Level 2 affords clients opportunities to invest in Charitable Gift Annuities. Contributions generally produce a charitable income tax deduction, but the value of this deduction is usually much lower than the value of the asset contributed. The charity sells the asset so no capital gain tax is due. Income payable to the client is based on the pre-sale contribution value. Distributions are partially tax-free because IRS guidelines allow for a pro rata return of principal and capital gain income (with calculations based on the sale price and the basis of the asset sold).

Level 3: The Charitable Remainder Trust ("CRT") resembles the Charitable Gift Annuity in some ways, but it is a more advanced Level Three strategy because of the increased ability for the client to influence the investment policy of the trust, grow the trust corpus tax-free at higher rates of return, and defer income for longer periods. By implementing a suitable asset management strategy, most distributions could be taxed as capital gain income. A 1031 Exchange does not generate an income tax deduction unless combined with a charitable strategy. The 1031 may allow a client to defer recognition of capital gain taxes if suitable like-kind property can be identified. A properly structured 1031 exchange allows a client to sell a property and reinvest the proceeds according to strict IRS guidelines. The new property will take the basis of the original property and gain will be deferred until the sale of the new property. This is a widely used strategy but it becomes less attractive when the real estate market is very strong because clients struggle to find a suitable new property. Moreover, a 1031 exchange does not work if the client wants to divest of real estate in order to spend the proceeds and/or redeploy assets in other types of investment vehicles.

Level 4: For years, estate planners have used Sales to Intentionally Defective Grantor Trusts ("IDGT") to "freeze" assets for estate planning purposes. A sale from a grantor to a grantor trust is generally exempt from capital gain tax. If the IDGT later sells assets, any capital gain recognized will be reportable by the grantor. This does not avoid the gain per se but it does permit the tax-free accumulation of capital in the trust because the grantor pays the tax. More advanced strategies, not depicted on the pyramid diagram above, may replace the Grantor Trust with a Non-Grantor Trust in order to defer capital gains taxes for more than 30 years; discussion of these advanced techniques goes beyond the scope of this article. More recently, new strategies relying on the installment sale rules have grown in popularity. These techniques involve the use of an intermediary who purchases the asset from the seller in exchange for a long-term installment contract. The intermediary immediately resells to the ultimate buyer. Purveyors of these strategies use different methods to address concerns sellers have about the use of installment sale transactions. For example, if a seller of a low basis asset wants to defer taxes using an installment contract but fears that the buyer may default on payment obligations, it may be possible to structure the arrangement so that the client receives a very high percentage of the asset sale value in cash shortly after closing, avoid the risk of intermediary default and defer the capital gain for 30 years.

Level 5: An Employee Stock Ownership Plan ("ESOP") can provide tax-free build-up of assets. When the ESOP is combined with a charitable trust, the resulting "ChESOP" can produce both tax deductions in the early years and tax-free income in later years. The ChESOP, by synergistically integrating features of charitable and non-charitable strategies, can produce tax-deductions in the early years, generate tax-free growth, and allow for tax-efficient distributions that are taxed at capital gains rates or are exempt from taxes. Pooled Income Funds ("PIF") have been offered by charities for many years but few clients find the benefits of a traditional PIF compelling. In recent years, however, donor-centric charitable organizations have begun to start new funds for a single family with a sufficient contribution of capital. The benefits can include a charitable income tax deduction in the 60%to 80% range, avoidance of capital gain tax and tax-favored distributions.

Level 6: Creative planners continue to find synergistic combinations of planning instruments that can provide benefits that exceed those illustrated in Level 5. For clients with significant charitable intent, a popular Level 6 strategy is the Charitable Limited Liability Company ("CLLC"). Notably, Mark Zuckerberg, founder of Facebook, recently announced a commitment to fund such a strategy with low basis stock. This strategy involves forming an LLC funded with highly appreciated assets. The client contributes nonvoting LLC interests to a suitable public charity. Following the contribution, the assets are sold in the LLC but the flow-through tax treatment of the LLC results in avoiding almost all capital gain tax. The client can serve as manager of the LLC and can control all the investments in the LLC without the restrictions that apply to private foundations (under IRC §§ 4941-4947). As long as the investments are managed in accord with various IRS guidelines, the manager of the LLC can engage in business activities, on an arm’s length basis, with the trustee of family trusts that benefit both entities. $1,000,000 contributed to this strategy may produce more than $4,000,000 for family and charity over time. This is complex strategy that must be managed carefully to avoid violating IRC §4958 and other rules regulating investment of charitable funds in transactions outside of the charitable foundation. Advisers are urged to have legal documents and investment policy statements reviewed by qualified professionals before implementing a Charitable Limited Liability Company.

Another Level 6 strategy is a Grantor Charitable Lead Annuity Trust ("CLAT"). This trust will pay income to charity for a specified term of years. At the end of the term, a family trust receives the assets remaining in the CLAT. A CLAT must be a grantor trust in order to generate a charitable income tax deduction. Structured properly, a "Super CLAT" generates a charitable income tax deduction and a gift tax deduction. The down-side of a typical grantor CLAT is that the earnings of the CLAT are taxable to the grantor annually. To overcome this problem, astute planners fund the Super CLAT with investments that grow tax-free, such as high-yield municipal bonds, leveraged real estate, or high cash value life insurance policies. When the CLAT is designed to make charitable distributions with tax-free income, the income taxable to the client can be reduced or eliminated. This can result in the client receiving large income tax deductions in the current year, tax-free growth of assets, tax-free payments during retirement or when transferring wealth to heirs, and larger gifts to favorite charities. The Super CLAT strategy can be used to offset taxes on Required Minimum Distributions ("RMDs") from retirement plans so that the clients losing retirement funds to income, IRD and estate taxes can instead leverage all retirement assets to benefit family and favorite charities.

While qualified attorneys opine that the above Level 6 strategies are within the letter and spirit of the tax code, the techniques may be too complicated for some clients. Moreover, attorneys must consider a long list of legal, tax, and financial issues when integrating the components of the advanced planning tools. Failure to implement and monitor strategies correctly can create unnecessary audit risks. If the client has concerns about the ability of his or her team to maintain a Level 6 strategy across time, then simpler strategies at Levels 2 to 5 may be better.

Conclusion

Tax laws are in a constant state of flux. Wise planners, like Hercules, find that each time Congress cuts the head off the hydra, two new heads grow. The decline in the demand for estate tax planning is small compared to the big increase in the demand for income tax and capital gain tax planning. Family office professionals have immense opportunities to serve the tens of millions of present and potential clients who are stuck in the entry levels of the tax-efficiency pyramid. As indicated above, there are compelling reasons and great financial rewards for the clients who advance to the higher levels of the tax-efficiency pyramid. Trained tax professional have great opportunities to provide leadership to clients who can benefit from the types of strategies discussed in this article.

About the Authors

Tim Voorhees, JD, MBA, AEP®. Throughout his 38-year career as an estate planning lawyer and investment adviser, Tim Voorhees' planning teams have developed thousands of "blueprints" that align legal, tax, and financial strategies with the vision and values of wealth holders. These plans have helped clients redirect billions of dollars of tax savings to trusts that generate greater after-tax retirement income, bigger transfers to family and larger gifts to favorite charities. See information about Tim's books at www.ZeroTaxCounsel.info, www.BestToolsManual.info, www.Legacies.info, and www.wisdom4wealthy.info. Tim regularly publishes articles in leading publications and speaks at conferences for many national organizations. To see a full bio, please visit www.TimVoorhees.com.

David Holaday, ChFC, CAP. Throughout his 30 years as a financial consultant, Dave has provided thought leadership as the author of numerous articles and creator of hundreds of comprehensive strategy illustrations. He has managed the case design, analysis, and presentation services for leading legal and financial firms that serve high net worth clients. Dave has a national reputation for developing unique and comprehensive solutions for complex family situations and often collaborates with the client’s existing tax, legal, insurance, and investment advisors. Dave cofounded The Wealth Design Center (a technology, training, and consulting firm), which was sold to a publicly-traded company. Dave also served as Director of Intellectual Property at Renaissance Inc., an Indianapolis-based provider of charitable consulting and trust administration services. To see a full bio, please visit www.vfos.com/Holaday.

Readers of this document should consult with independent advisors regarding the tax, accounting and legal implications of the proposed strategies before any strategy is implemented. Nothing in this presentation is intended to offer securities or investment advice. Tax and regulatory rules affecting strategies in this document may change often and have varying interpretations. To ensure compliance with requirements imposed by the IRS under Circular 230, we inform you that any U.S. federal tax advice contained in this communication is not intended or written to be used, and cannot be used, for the purpose of avoiding penalties under the Internal Revenue Code or for promoting, marketing or recommending to another party any matters addressed herein.